Subscription fraud doesn’t act like fraud—that’s why most systems miss it. It’s no longer flagged cards or flash-sale spikes—it’s ghosted free trials, promo stacking, and coordinated device spoofing that mimic actual user behavior.

I’m Divesh Singh Sai, a Senior Software Engineer with over a decade of experience building fraud prevention systems for high-scale digital payment platforms—where every millisecond counts and every transaction could be a risk.

Don’t want to miss the best from TechLatest?

Set us as a preferred source in Google Search

and make sure you never miss our latest.

In this article, I’ll explain how we built adaptive fraud defenses for subscription payments using supervised learning, anomaly detection, and behavioral modeling.

If you’re building fraud systems at scale—or trying to understand how AI uncovers threats hidden in plain sight—this guide will give you the technical patterns and strategies that work in production.

How My Work Sparked a Focus on Subscription Fraud

My interest in AI-powered fraud detection didn’t start in theory—it started in production.

While working on payment services, I took on the challenge of improving the platform’s ability to detect unusual payment behavior.

The project began with rule-based systems, where we flagged transactions using predefined conditions: multiple failed payments, unusual device locations, or rapid account switching.

However, as the service scaled globally and the fraudsters became more sophisticated, those static rules became liabilities.

One standout example is when we noticed a surge in free trial misuse. Users created multiple accounts across devices and regions, exploiting promotional codes and regional pricing gaps.

Because these actions didn’t violate any individual rule, they slipped through the cracks. That’s when we saw how quickly rules became liabilities.

In response, I helped lead initiatives that used AI and ML to catch more nuanced patterns. We implemented fraud screening layers capable of tracking behavior across accounts and devices, identifying anomalies that weren’t obvious at the individual transaction level.

This transformation, which spanned browser, TV, and mobile platforms, pushed me to explore cutting-edge ML techniques—especially those that could operate in real-time and handle massive data volumes.

Why Traditional Systems Fall Short in Subscription Fraud Detection

Developers originally designed conventional fraud detection methods—like static rule engines, statistical models, and blocklists—for more straightforward use cases.

These methods work well when patterns are predictable, such as detecting a sudden spike in transaction volume or a suspicious IP address.

However, subscription services introduce ongoing relationships between users and platforms, meaning fraudulent behavior is often stretched over time and disguised as regular activity.

For example, a fraudster might use a stolen card to start a subscription, consume content, and initiate a chargeback a month later.

Or they might take over a legitimate account, change the payment method, and quietly add several add-on subscriptions. Rule-based systems often miss these slow-burn attacks because they rely on immediate red flags rather than behavioral trends.

I encountered this firsthand while working on fraud prevention systems. We had cases where bad actors manipulated subscription renewals, trial windows, and device limits in ways that weren’t detectable with rules alone.

These failures frustrated users and eroded customer trust, often triggering unnecessary support interventions.

This wasn’t just our experience. An SSRN paper about artificial intelligence in financial services highlights the inability of static systems to adapt to evolving fraud techniques. These findings strongly align with what I observed in practice.

How We Use AI to Catch Fraud, You’ll Never See Coming

“Much of what we do with machine learning happens beneath the surface. Machine learning drives our algorithms for demand forecasting, product search ranking, product and deals recommendations, merchandising placements, fraud detection, translations, and much more.” — Jeff Bezos, via Four.co.uk

This quote reflects what I saw firsthand in my work. The most effective machine learning systems often operate quietly in the background—but they’re critical, especially in fraud detection.

In subscription payment systems, we saw that no single algorithm could solve the complexities of subscription fraud. We shifted from static rule-based systems to layered, ML-driven approaches, each addressing a different fraud pattern.

This enabled us to detect behavior-based anomalies in real-time rather than relying on predictable rule triggers.

Supervised Learning for Fraud Detection

Supervised learning played a foundational role in our fraud pipeline. We used algorithms such as Decision Trees, Random Forests, and Gradient Boosting Machines to classify transactions based on known fraud patterns.

We trained these models on labeled data—cases we had already identified as fraudulent or legitimate—and used them to spot repeat behaviors like subscription stacking and payment method testing long before human review could.

A study by GSCARR supports this approach, showing that supervised models significantly reduce false positives and improve fraud detection precision in high-volume platforms like digital banking and streaming services.

Unsupervised Learning for Anomaly Detection

Some fraud doesn’t repeat. It mutates.

We turned to unsupervised learning, using methods like Autoencoders, K-Means Clustering, and Isolation Forests to identify anomalies without requiring labeled data.

These models helped surface emerging threats, such as coordinated promo abuse—by spotting outliers in behavior, like repeated trial signups from slightly altered device IDs.

A research paper published by ESP-IJACT showed that these unsupervised models reduced manual fraud review by catching previously unseen fraud signals that conventional systems often miss.

Real-Time Detection with Deep Learning

Deep learning was essential for handling complex, time-sequenced behaviors in real-time. We used Recurrent Neural Networks (RNNs) and Convolutional Neural Networks (CNNs) to monitor user actions over time, tracking how users browsed, subscribed, switched devices, or logged in from new regions.

These models processed user journeys—login, browse, subscribe, switch devices, cancel—and flagged anything that broke the expected flow.

According to IJFMR, deep learning models can deliver sub-50ms inference speeds in production, allowing fraud detection without introducing latency into the user experience. This performance matched our experience deploying models through AWS Lambda for real-time inference.

Behavioral Analytics and User Profiling

Another key layer of detection came from behavioral analytics. We used hidden Markov Models (HMMs) and Long Short-Term Memory (LSTM) networks to profile user behavior over time.

We profiled behavior across login patterns, device habits, and session lengths. This helped us spot differences between real users and fraudsters, especially those hiding behind VPNs or emulators.

Behavioral modeling was especially critical in protecting user accounts across streaming devices and platforms, where fraudulent activity often closely mirrored legitimate user behavior.

Graph-Based Fraud Detection

To detect coordinated fraud, we introduced Graph Neural Networks (GNNs). These models mapped relationships between users, devices, IP addresses, and payment methods.

In one instance, we uncovered a fraud ring exploiting promo codes by linking dozens of seemingly unrelated accounts that shared payment fingerprints and device IDs.

This graph-based approach helped reveal large-scale, organized abuse, often invisible to traditional rules-based systems. It became one of the most impactful upgrades to our detection stack, especially in a subscription environment where bad actors collaborate to bypass platform limits.

What It Takes to Run AI Fraud Detection at Scale

Translating AI models from theory to practice was a core part of my work in subscription payment systems.

Beyond selecting the right models, we needed to ensure our systems could operate at scale, handle massive data volumes, and deliver real-time insights, without interrupting the customer experience.

This involved everything from feature engineering to cloud-based deployment and constant iteration based on live data.

Data Collection and Feature Engineering

We built our fraud models on high-quality data. We collected various metadata, such as transaction value, timestamps, IP geolocation, device ID, and user behavior across sessions and devices. For subscription-specific insights, we engineered features like:

- Transaction velocity across short windows

- Device usage consistency across accounts

- Payment method lifespan and switching behavior

- Subscription lifecycle patterns (e.g., reactivations after free trials)

As part of enterprise-grade engineering and compliance standards, we also ensured that this data remained anonymized and compliant with internal privacy policies and regional regulations.

Model Training and Evaluation

In my role leading fraud detection initiatives, I translated business signals into scalable, model-ready features to support fraud detection.

We worked with large volumes of production transaction data enriched by metadata, capturing behavioral indicators like device consistency, payment switching frequency, and promo code usage.

I aligned our signals with actual subscription abuse, such as trial recycling and coordinated promo stacking. These insights informed the models we deployed in our payment screening systems.

Leveraging contextual features from user behavior, rather than relying solely on transaction values, significantly improves the performance of AI-based fraud detection.

After deployment, we closely monitored how models performed in live environments. I focused on ensuring the fraud pipeline aligned with product experience goals, adapting as user behavior and fraud patterns evolved. This helped us ensure strong fraud coverage while preserving a seamless experience for legitimate users.

Integration with Payment Systems

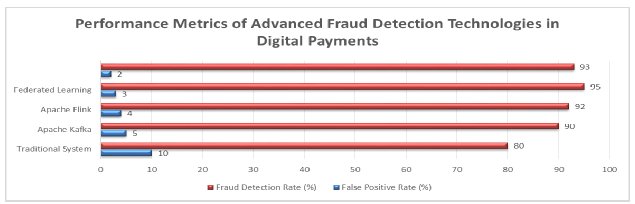

Fraud detection also had to work in real-time. We deployed models into production using the following:

- AWS Lambda, for rapid inference

- DynamoDB, to store and retrieve risk scores

- Microservices and APIs for routing flagged cases

- Kafka, for streaming and scaling across regions

This architecture ensured our system could flag threats before the transaction was completed while remaining invisible to everyone but the fraudster.

Continuous Learning and Adaptation

Fraudsters evolve, and so must our systems. We implemented feedback loops that ingested analyst-confirmed fraud cases and adjusted model behavior accordingly.

In select projects, we also explored reinforcement learning approaches that optimized not just for fraud catch rate but for minimizing long-term false positives.

Future Trends in AI-Driven Fraud Prevention

Innovations prioritizing transparency, collaboration, and data integrity are shaping the future of fraud detection while maintaining the speed and scale demanded by subscription platforms.

Explainable AI (XAI)

The hardest part of AI isn’t building it. It’s explaining why it made a decision.

Stakeholders—from compliance officers to customer service teams—must understand why a transaction was flagged. Explainable AI allows us to provide the reasoning behind each fraud decision.

According to Science Times (2024), the demand for transparent AI models is accelerating, with institutions seeking tools supporting regulatory compliance and customer trust.

Federated Learning

In global organizations, data is often siloed or governed by regional privacy laws. Federated learning addresses this by training models across distributed data sources without moving the data. It makes collaborative fraud defense possible while safeguarding user privacy.

It’s a model we’ve begun to explore within large-scale systems to strengthen fraud signals across services, without exposing or centralizing sensitive user data.

Blockchain-Based Fraud Prevention

While still emerging, blockchain offers compelling potential for securing transaction integrity. Using decentralized ledgers ensures that each transaction is verifiable, tamper-proof, and traceable—vital in preventing identity-based subscription fraud and digital asset theft.

Where Subscription Fraud Is Going Next (And How to Prepare)

Fraud in subscription-based digital payments is growing and becoming more sophisticated. From free trial abuse to social engineering, fraudsters rapidly evolve their tactics.

In my work leading fraud screening for subscription payment platforms, I saw firsthand how traditional systems fall short and how AI and machine learning can transform detection.

Using supervised and unsupervised learning approaches, behavioral modeling, and graph analysis, we built scalable solutions that adapt in real time.

However, effective fraud prevention requires more than just innovative tools. It takes vision—vision to create adaptive, transparent systems that protect both customers and business outcomes.

If you’re waiting to act, you’re already behind.

References:

- Adaboina, S.R., (2024). AI and ML in Fraud Detection: How Algorithms Are Catching Criminals. Science Times. https://www.sciencetimes.com/articles/60131/20241216/ai-ml-fraud-detection.htm

- Chopra, P. and Binwal, A., (2024). Enhancing Security and Fraud Detection in Digital Payments Using Machine Learning. International Journal for Multidisciplinary Research, 6(6). https://www.ijfmr.com/papers/2024/6/30337.pdf

- Mahapatra, B.G., (2024). AI and Machine Learning in Fraud Detection. ESP International Journal of Advancements in Computational Technology, 2(4), pp.125–139. https://www.espjournals.org/IJACT/2024/Volume2-Issue4/IJACT-V2I4P117.pdf

- Olowu, O., Adeleye, A.O., Omokanye, A.O., Ajayi, A.M., Adepoju, A.O., Omole, O.M. and Chianumba, E.C., (2024). AI-driven fraud detection in banking: A systematic review of data science approaches to enhancing cybersecurity. GSC Advanced Research and Reviews, 21(2), pp.227–237. https://gsconlinepress.com/journals/gscarr/sites/default/files/GSCARR-2024-0418.pdf

- Patil, D., (2024). Artificial Intelligence in Financial Services: Risk Management and Fraud Detection. SSRN Electronic Journal. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5057412

This story was originally published on 14 August 2024.

Enjoyed this article?

If TechLatest has helped you, consider supporting us with a one-time tip on Ko-fi. Every contribution keeps our work free and independent.

Support on Ko-fiDirectly in Your Inbox